Can You Create Your Own Pension in Retirement?

For many retirees, one of the most valuable features of a traditional pension is the confidence it provides. A pension delivers predictable income month after month, helping retirees cover expenses without worrying about market fluctuations or outliving their savings.

Today, fewer Americans have access to employer-sponsored pensions, but that doesn’t mean guaranteed lifetime income is out of reach. Certain annuity products can help create a “personal pension” by providing a guaranteed stream of income that lasts throughout retirement.

Why Guaranteed Income Matters

Retirement planning is about more than simply accumulating assets. While a portfolio of savings and investments is important, many retirees find it comforting to know that a portion of their income is guaranteed regardless of what happens in the markets.

A guaranteed income strategy may help address several common retirement concerns:

- Longevity Risk – The possibility of outliving your savings.

- Sequence of Returns Risk – The impact of poor market performance early in retirement.

- Spending Confidence – Knowing you have dependable income can make it easier to enjoy retirement and spend with greater peace of mind.

How Income Riders Work

Some fixed annuities offer a Guaranteed Income Rider, which allows you to receive a guaranteed withdrawal amount for life. The percentage available typically increases with age, reflecting a shorter expected payout period.

Current industry withdrawal rates may look similar to the following:

Individual Lifetime Income:

| Age | Withdrawal Rate |

| 60 | 7.0 0% |

| 65 | 7.60% |

| 70 | 8.35% |

| 75 | 8.80% |

| 80 | 9.05% |

Joint Lifetime Income:

| Age (Both Spouses) | Withdrawal Rate |

| 60 | 6.50% |

| 65 | 7.10% |

| 70 | 7.85% |

| 75 | 8.30% |

| 80 | 8.55% |

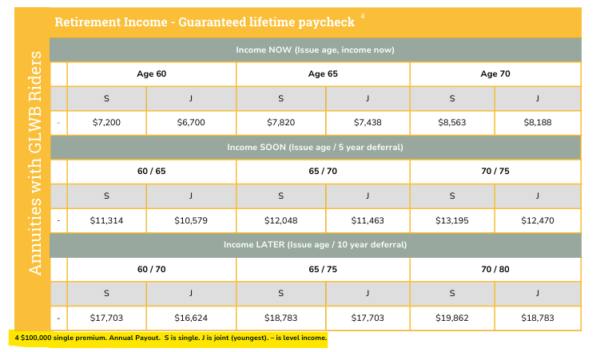

Example Lifetime Paycheck:

Is a Personal Pension Right for You?

Every retirement plan is unique. For some individuals, guaranteed lifetime income can serve as a foundation for essential expenses, while investment assets remain available for growth, emergencies, or legacy planning.

The right balance between guaranteed income and investment flexibility depends on your goals, income needs, and overall financial situation.

If you’d like to learn more about how guaranteed income strategies fit into a retirement plan, give us a call. We’d be happy to discuss your options and help you determine whether a personal pension strategy makes sense for your retirement goals.

-Preston French, Managing Partner

W&A Advanced Markets Group

License #2371878

###